August 6, 2025-

No Comments

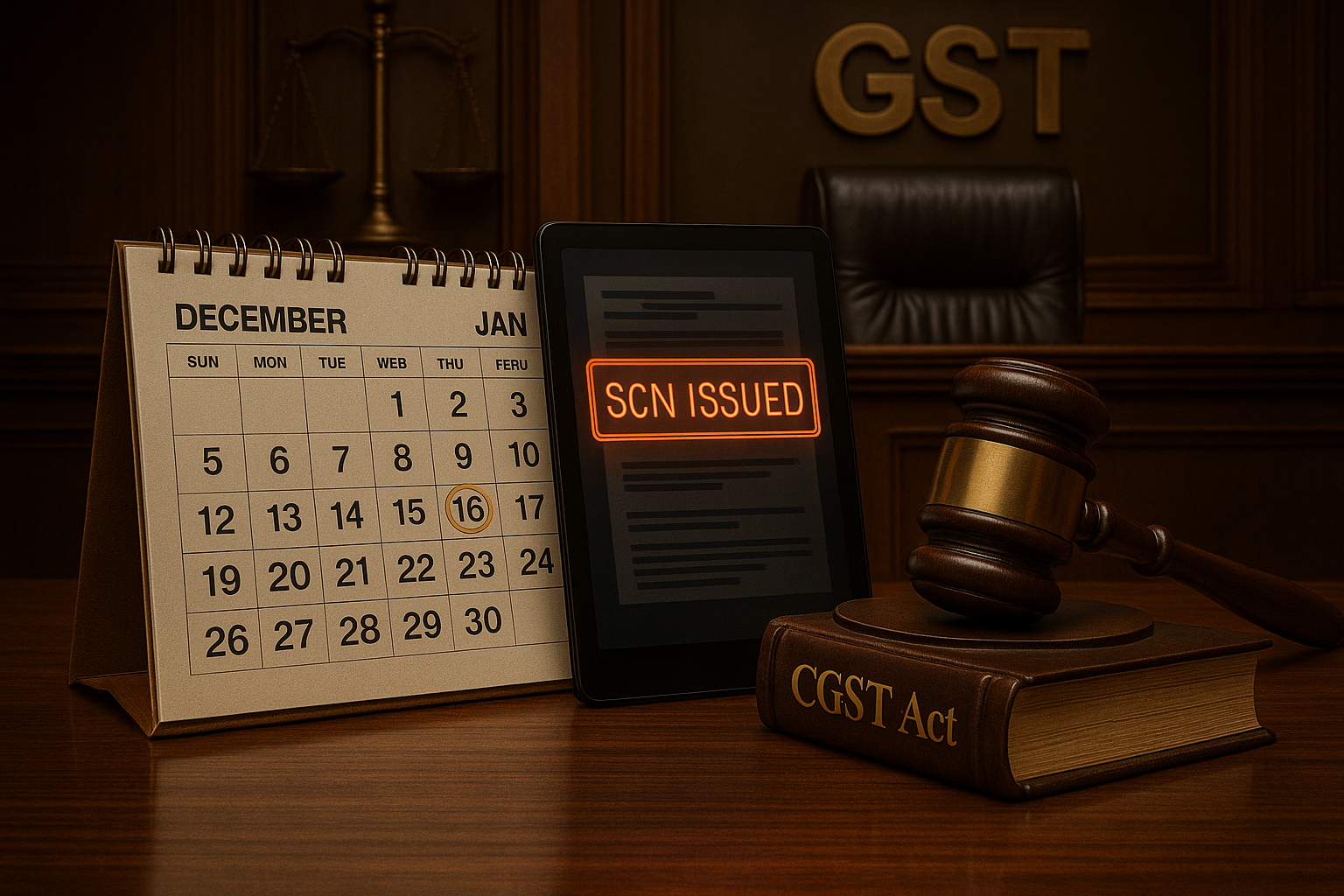

In a landmark decision, the Delhi High Court has clarified a key procedural aspect under the Goods and Services Tax (GST) regime. The Court held that the phrase “three months” used in Section 73(2) of the CGST Act must be interpreted as three calendar months and...