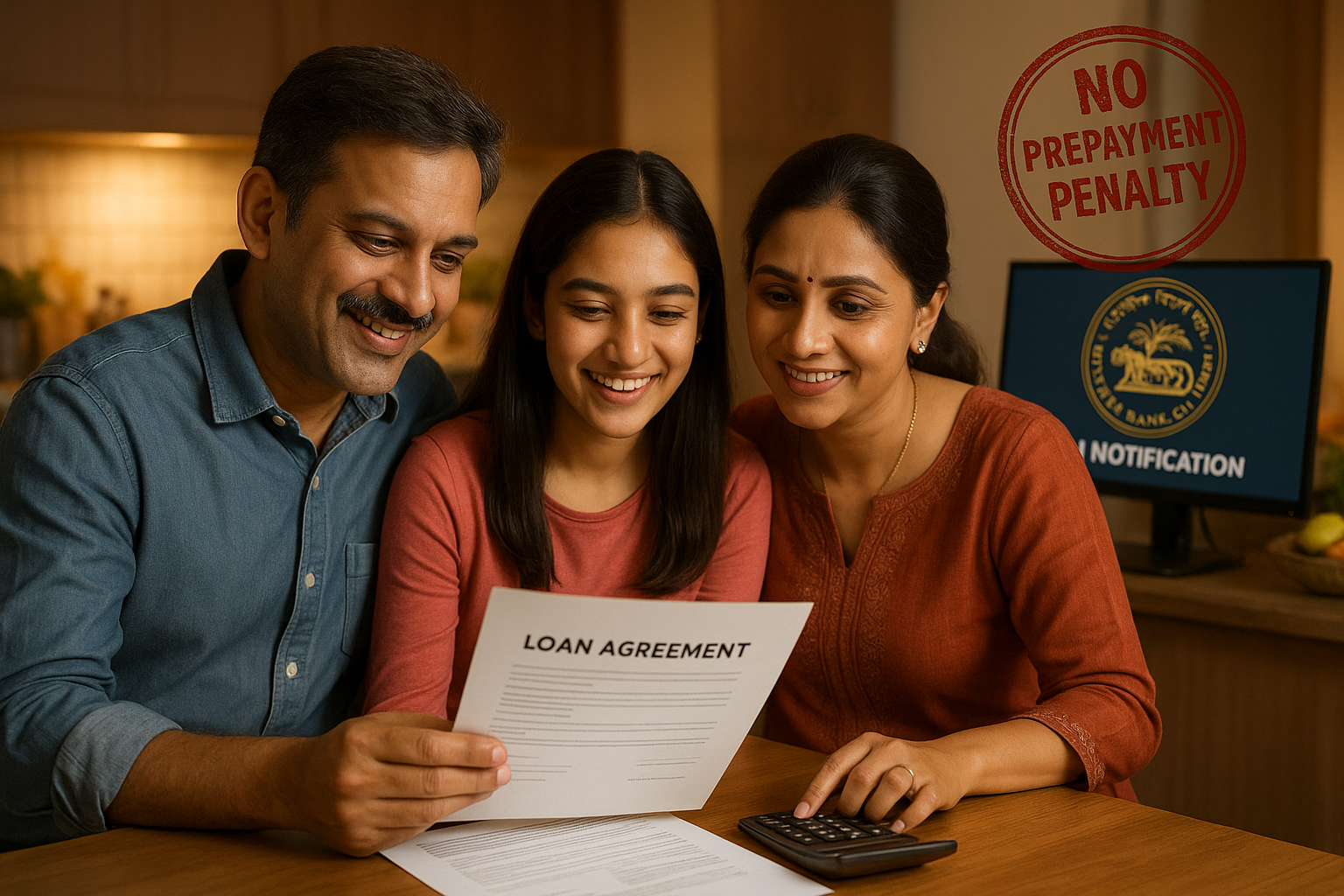

Starting January 1, 2026, borrowers across India will have more control over their loan repayments. The Reserve Bank of India (RBI) is all set to implement a set of borrower-friendly guidelines aimed at enhancing transparency and protecting consumers from hidden charges and unfair loan practices—especially around loan prepayments and foreclosure penalties.

What’s Changing?

Under the new framework, borrowers will be allowed to prepay or foreclose their loans without facing punitive charges, especially in cases where:

-

The loan is floating rate in nature (i.e., interest rate can change over time)

-

The repayment is being made from borrower’s own funds

-

Prepayment is being done partially or fully before the scheduled tenure

This change is being seen as a major win for retail borrowers, particularly those with home loans, personal loans, and education loans.

“Prepayment is a financial right, not a revenue opportunity for lenders,” says CA Manish Mishra, an independent financial advisor.

Why It Matters

Many borrowers have long felt trapped by clauses that discouraged early repayments through:

-

Prepayment penalties (as high as 2–3% of outstanding balance)

-

Complicated loan documents that didn’t clearly disclose such charges

-

Lack of parity between floating and fixed-rate treatment

These new rules ensure greater borrower empowerment, particularly in an interest rate cycle where people aim to prepay faster to save on overall interest outgo.

Who Benefits?

-

Home loan borrowers with long tenures looking to reduce interest burden

-

Education loan holders receiving funds through scholarships or jobs

-

Personal loan customers repaying from bonuses, windfalls, or savings

-

Senior citizens or retirees aiming to close loans with retirement corpus

Industry Reaction

Banks and NBFCs have shown mixed reactions. While public sector banks largely comply with RBI’s earlier advisories, many private lenders and NBFCs charge fees for early closures, especially on unsecured loans.

“The guidelines create a level playing field and reduce friction in financial planning,” says Manoj Kumar Singh, a banking policy expert.

What Should Borrowers Do Now?

-

Check your loan agreement for existing prepayment clauses

-

Monitor communications from your lender by December 2025

-

Plan your repayment strategy to align with January 1, 2026 rollout

-

Inquire if refunds are due in cases where prepayment charges were levied against floating rate norms

RBI’s Larger Goal

This is part of a broader RBI push to improve customer transparency and fair practices in retail lending. From tightening digital lending rules to mandating clear disclosures, the central bank is steadily moving toward a borrower-first ecosystem.

Conclusion

With these new prepayment norms taking effect in January 2026, borrowers will finally have greater flexibility, fewer hidden costs, and more power over their loan journey. For India’s growing middle class and financially aware citizens, it’s a step toward financial freedom and responsible credit behavior.