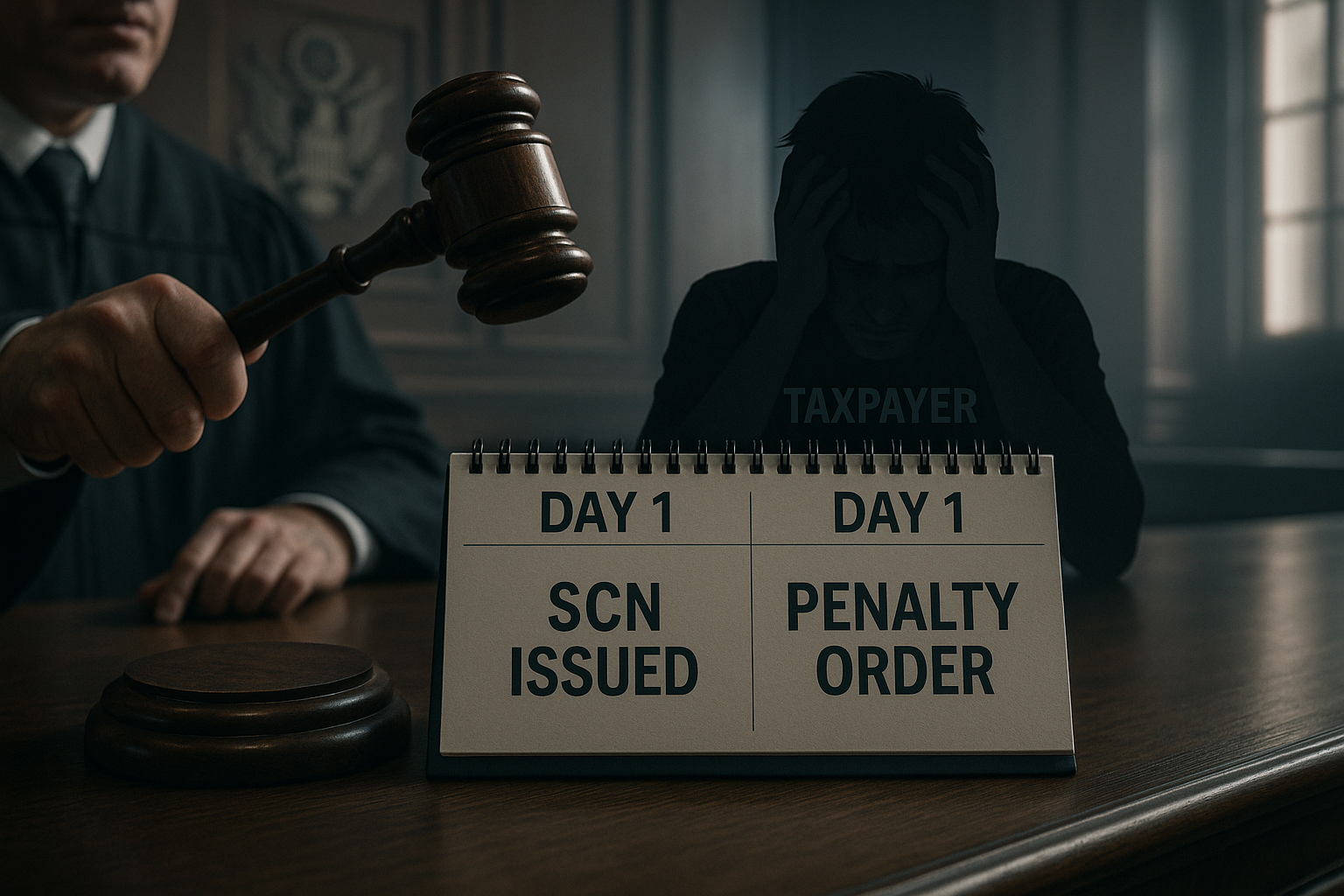

Several Indian High Courts have recently invalidated penalty orders issued on the same day a Show Cause Notice (SCN) was served—without providing the accused an opportunity to respond. This recurring judicial intervention reinforces that natural justice (audi alteram partem) is non-negotiable, even when legal deadlines are tight or authorities aim for expedited conclusions.

Background: The Principle of “Audi Alteram Partem”

At the heart of administrative and judicial fairness lies the principle of “hear the other side”—a pillar of constitutional law in India. Issuing an SCN and passing a penalty order simultaneously blindsides the taxpayer or litigant, offering no chance to defend, clarify, or mitigate. Courts across tax regimes have repudiated such procedural shortcuts, citing them as violative of basic rights.

Key Judicial Rulings

Himachal Pradesh High Court

An assessment followed an accelerated penalty notice process:

-

SCN served, hearing held, and order passed within 48 hours, a timeline deemed unreasonable.

-

Court quashed the order for denying the accused adequate time to prepare a meaningful response.

[Reference: Himachal Pradesh High Court decision]

Allahabad High Court (GST Regime)

A taxpayer challenged a GST penalty under Section 125 where:

-

SCN, hearing, and order all occurred on the same day.

-

The Court struck down the penalty, calling it a violation of fundamental rights.

[Reference: Kahna Bartan Bhandar case, Allahabad HC]

Tax Courts & Other High Courts

Multiple rulings across tax jurisdictions (CGST, GST, Income Tax) underscore the illegitimacy of same-day procedures—agreeing consistently with higher-court precedents.

[References: TaxGuru, Taxmann, etc.]

Implications for Stakeholders

| Stakeholder | Implication |

|---|---|

| Taxpayers/Assessees | Must be afforded reasonable response time post-SCN—advocates or personal replies should be considered valid. |

| Tax Authorities | Required to revise internal timelines to ensure sufficient gap between SCN and order. |

| Legal Practitioners | Should challenge orders passed without genuine hearings; reference judicial precedence. |

Why This Matters

-

Preservation of Legal Rights: SCN-process systems built for audits, penalties, and probes must prioritize fairness—speed cannot come at the cost of rights.

-

Judicial Continuity: These rulings reaffirm consistent jurisprudence across multiple High Courts, cementing procedural fairness as a non-negotiable norm.

-

Policy Fixation: Regulatory authorities should revise circulars and SOPs to eliminate the practice of expedited penalty imposition without genuine notice.