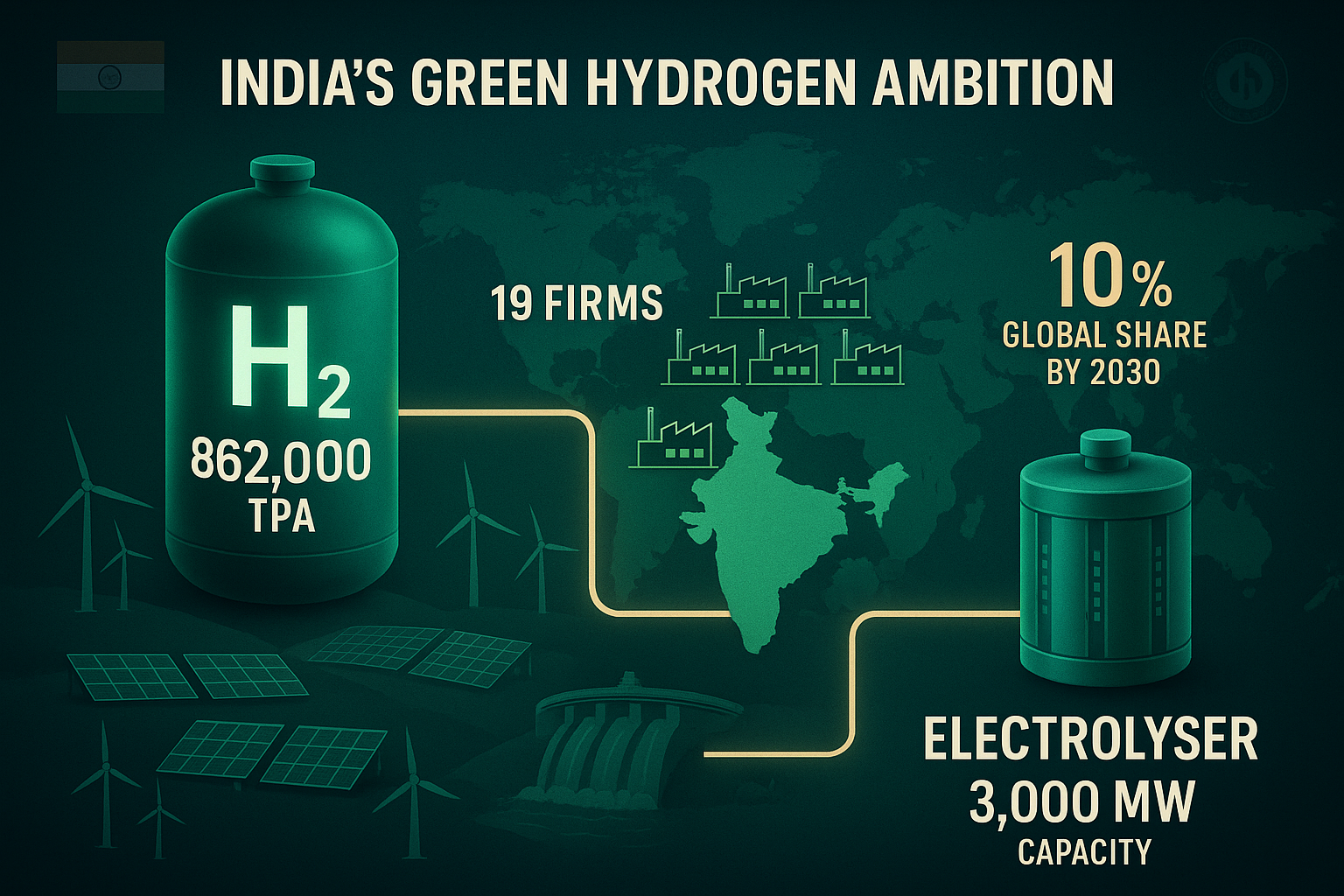

India has set its sights on capturing 10% of global green hydrogen demand by 2030, with production expected to exceed 100 million tonnes worldwide. At the FICCI Green Hydrogen Summit 2025, the government announced the allocation of 862,000 tonnes per annum (TPA) of production capacity across 19 companies, alongside 3,000 MW of electrolyser manufacturing capacity to 15 firms. Backed by its growing renewable energy base, India is positioning itself as a future hub for green hydrogen exports, aligning industrial strategy with climate goals.

Production & Electrolyser Allocation

862,000 TPA of green hydrogen production capacity allocated to 19 companies.

3,000 MW electrolyser manufacturing capacity awarded to 15 firms under the National Green Hydrogen Mission.

This dual allocation builds both supply-side manufacturing and production infrastructure, ensuring scalability.

Renewable Energy Backbone

India’s transition is supported by robust clean energy growth:

237 GW total renewable capacity (as of June 2025)

Solar: 119 GW

Wind: 52 GW

Hydro: 49 GW

8.78 GW nuclear capacity also contributes to non-fossil energy.

Over 50% of India’s installed power capacity is now non-fossil-based, creating the foundation for large-scale hydrogen production.

Cost Competitiveness Emerges

Industry experts highlighted that in recent international bids, green hydrogen prices undercut blue hydrogen, marking a global inflection point. India’s scale and resource base could make it one of the lowest-cost producers globally.

International Partnerships

India is building global frameworks to support exports:

Creation of an India-EU Hydrogen Task Force for technology and trade alignment.

Push for bilateral cooperation with markets in Europe, Japan, and South Korea, which have rising clean fuel demand.

R&D & Innovation Ecosystem

The mission also prioritizes innovation:

Over 23 R&D projects funded to accelerate electrolyser efficiency and hydrogen storage.

More than 100 Centre of Excellence proposals received to create long-term institutional capacity.

Why This Matters

Export Leadership: Aiming for 10% of global hydrogen demand positions India as a leading clean energy exporter.

Energy Transition: Moves India closer to its net-zero 2070 target, reducing reliance on fossil fuels.

Industrial Competitiveness: Lower-cost hydrogen offers an edge to Indian steel, fertilizer, and refining industries.

Policy Momentum: Strong government backing through PLI schemes, auctions, and fiscal incentives builds market confidence.

Global Integration: International partnerships open pathways for trade, finance, and advanced technology transfer.