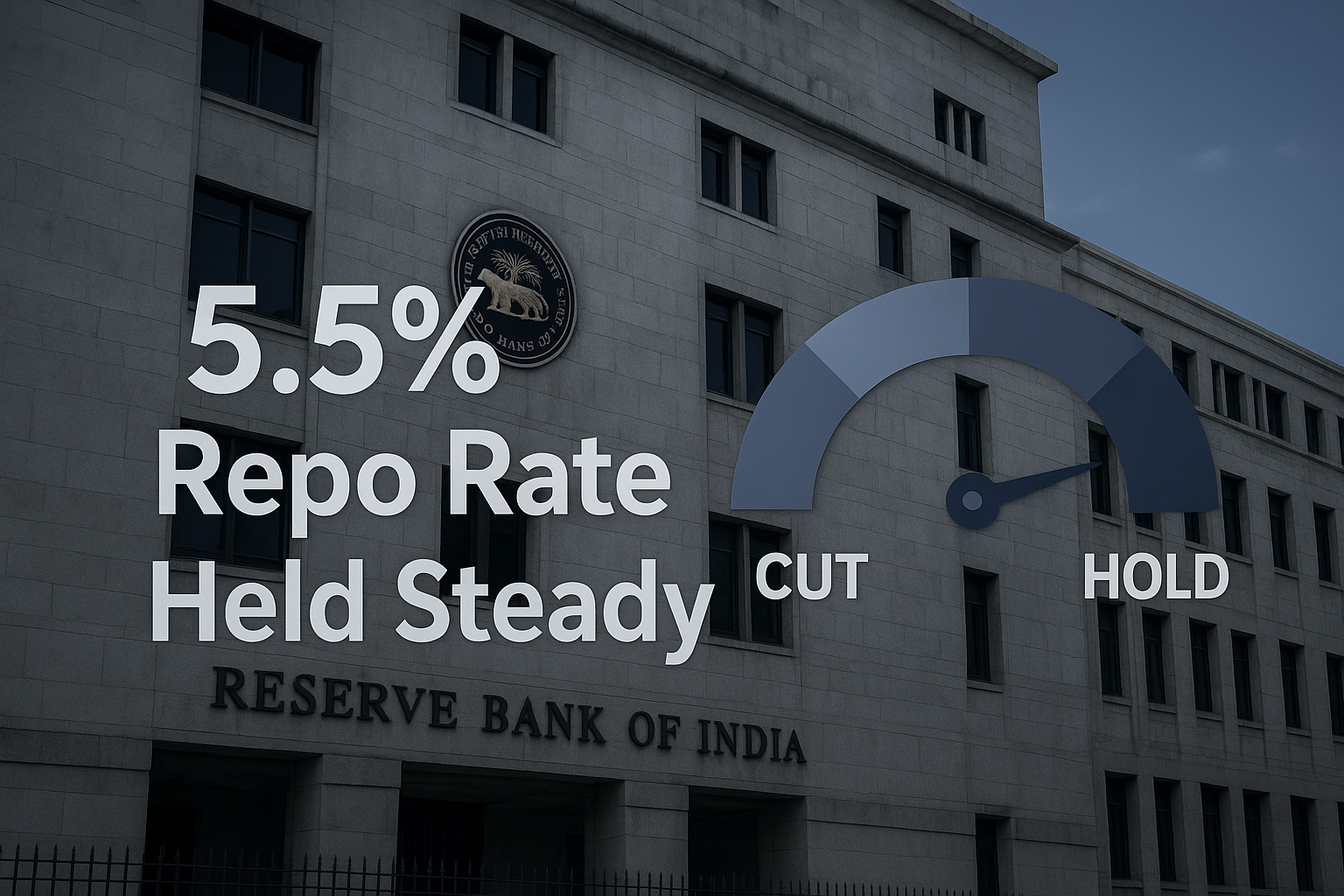

The State Bank of India (SBI) characterizes the RBI’s decision to hold the repo rate at 5.5% as a “technical pause.” With inflation projected to stay below 3% through Q3 FY26 and likely to rise sharply to 4.9% in Q1 FY27, SBI notes that this may well be the terminal rate, significantly narrowing space for further cuts in 2025.

Background & Rationale

The RBI’s Monetary Policy Committee (MPC), led by Governor Sanjay Malhotra, maintained the repo rate at 5.5%, keeping its policy stance ‘neutral.’ This follows cumulative cuts of 100 basis points earlier in the year, signaling confidence in moderating inflation even amid global uncertainties.

SBI’s Analysis & Key Takeaways

| Metric | Observation |

|---|---|

| Inflation Trend | Below 3% till Q3 FY26; projected to rebound to 4.9% in Q1 FY27, limiting cut space. |

| Scope for 2025 Rate Cuts | Minimal — only marginal relief (up to 25 bps) if inflation undershoots projections. |

| Economic Growth Outlook | Strong growth expected into H1 FY26—boosting confidence for a rate hold. |

| Policy Outlook | Neutral stance indicates RBI is watching incoming data and staying fluid. |

Broader Analyst Verdict

Citi maintains the terminal repo rate at 5.5%, citing constrained inflation/growth balance.

RBI’s Technical Pause: Rather than signaling a shift to tightness, the decision indicates a strategy pause to gauge real-time data.

Fixed-Income Outlook: This pause generates opportunity for bond investors—offering steadier yield expectations and potential price appreciation.

What Lies Ahead for 2025?

Limited Cuts Expected: Most economists and SBI anticipate no further rate cuts unless unexpected economic shocks surface.

Data-Dependent Strategy: Future decisions will hinge on inflation trends, GDP performance, monsoon patterns, and global headwinds.

Festival Season Watch: Demand upticks may factor into RBI’s next policy decision, though expectations are cautiously grounded.

Final Thoughts

The RBI’s latest policy signalling can be described as neutral and measured, with SBI suggesting this may be the cyclical bottom for repo rates, barring unforeseen disruptions. For markets and debt investors, this means stability—but also the need for vigilance. Further easing in 2025 appears unlikely unless inflation weakens significantly or growth falters.